Small Business Payroll Calculator — Budget Payroll Taxes (2026)

Calculate payroll tax costs for your small business. See exactly how much you'll pay in employer taxes (FICA, FUTA, SUI) per employee and budget your total payroll expenses accurately.

Employer Payroll Tax Rates for 2026

| Tax | Rate | Wage Base | Notes |

|---|---|---|---|

| Social Security (OASDI) | 6.2% | $184,500 | Employer match |

| Medicare (HI) | 1.45% | No cap | Employer match |

| FUTA | 0.6% | $7,000 | After state credit |

| State Unemployment (SUI) | 0.5–8.5% | Varies | Based on experience rating |

| Total Employer FICA | 7.65% | — | SS + Medicare combined |

Employer Tax Cost Per Employee

Here's the minimum employer payroll tax cost (before SUI) at different salary levels:

| Employee Salary | Employer SS | Employer Medicare | FUTA | Total Employer Tax | % of Salary |

|---|---|---|---|---|---|

| $30,000.00 | $1,860.00 | $435.00 | $42.00 | $2,337.00 | 7.79% |

| $40,000.00 | $2,480.00 | $580.00 | $42.00 | $3,102.00 | 7.75% |

| $50,000.00 | $3,100.00 | $725.00 | $42.00 | $3,867.00 | 7.73% |

| $60,000.00 | $3,720.00 | $870.00 | $42.00 | $4,632.00 | 7.72% |

| $75,000.00 | $4,650.00 | $1,087.50 | $42.00 | $5,779.50 | 7.71% |

| $85,000.00 | $5,270.00 | $1,232.50 | $42.00 | $6,544.50 | 7.7% |

| $100,000.00 | $6,200.00 | $1,450.00 | $42.00 | $7,692.00 | 7.69% |

| $120,000.00 | $7,440.00 | $1,740.00 | $42.00 | $9,222.00 | 7.69% |

Total Payroll Budget by Team Size

Estimate your annual payroll budget based on team size (average salary: $55,000, avg SUI rate: 2.7%):

| Team Size | Total Salaries | Employer FICA+FUTA | Est. SUI | Total Annual Cost |

|---|---|---|---|---|

| 1 employee | $55,000.00 | $4,249.50 | $1,485.00 | $60,734.50 |

| 3 employees | $165,000.00 | $12,748.50 | $4,455.00 | $182,203.50 |

| 5 employees | $275,000.00 | $21,247.50 | $7,425.00 | $303,672.50 |

| 10 employees | $550,000.00 | $42,495.00 | $14,850.00 | $607,345.00 |

| 15 employees | $825,000.00 | $63,742.50 | $22,275.00 | $911,017.50 |

| 25 employees | $1,375,000.00 | $106,237.50 | $37,125.00 | $1,518,362.50 |

| 50 employees | $2,750,000.00 | $212,475.00 | $74,250.00 | $3,036,725.00 |

Small Business Payroll Checklist

Getting Started

- ✅ Get an EIN (apply online)

- ✅ Register with your state for unemployment insurance (SUI)

- ✅ Have employees complete W-4 (federal) and state withholding forms

- ✅ Verify employment eligibility (Form I-9)

- ✅ Set up a payroll schedule (weekly, bi-weekly, semi-monthly, or monthly)

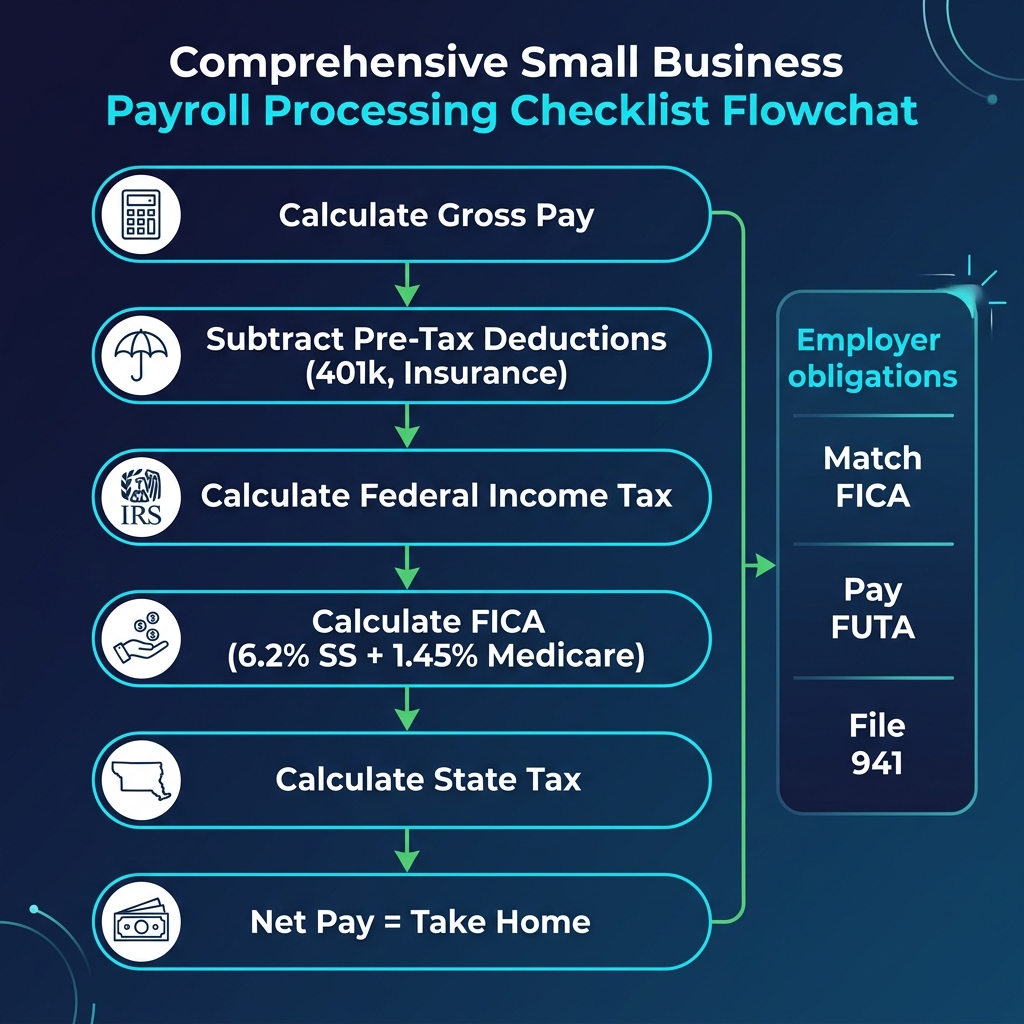

Each Pay Period

- Calculate gross pay (salary ÷ pay periods, or hours × rate)

- Subtract pre-tax deductions (401k, health insurance)

- Calculate and withhold federal income tax (2026 brackets)

- Calculate and withhold state income tax (state calculators)

- Withhold employee FICA (6.2% SS + 1.45% Medicare)

- Set aside employer FICA match (another 7.65%)

Tax Deposits Source: IRS.gov

- Monthly depositors: Deposit by the 15th of the following month

- Semi-weekly depositors: Deposit within 3 business days of payday

- FUTA: Deposit quarterly if liability exceeds $500

Annual Filings

- Form 941 — Quarterly federal tax return

- Form 940 — Annual FUTA tax return

- W-2s — To employees by January 31

- W-3 — To SSA by January 31

- State filings — Vary by state

Tips to Reduce Payroll Costs

- Hire in no-income-tax states — Remote workers in Texas, Florida, or Washington save employees on state tax (though employer SUI still applies)

- Maximize Section 125 plans — Pre-tax health insurance reduces FICA for both you and employees

- Consider S-Corp structure — S-Corp owners can pay reasonable salary + distributions to minimize SE tax

- Use the Work Opportunity Tax Credit (WOTC) — Up to $9,600 credit per qualifying new hire

- Claim FICA Tip Credit — Restaurant owners can credit employer FICA on tips above minimum wage

Small Business Payroll FAQ

Related Tools