S-Corp Payroll Calculator — Reasonable Salary & Tax Savings (2026)

Calculate the optimal owner salary for your S-Corporation and see how much you can save in self-employment taxes compared to a sole proprietorship or single-member LLC.

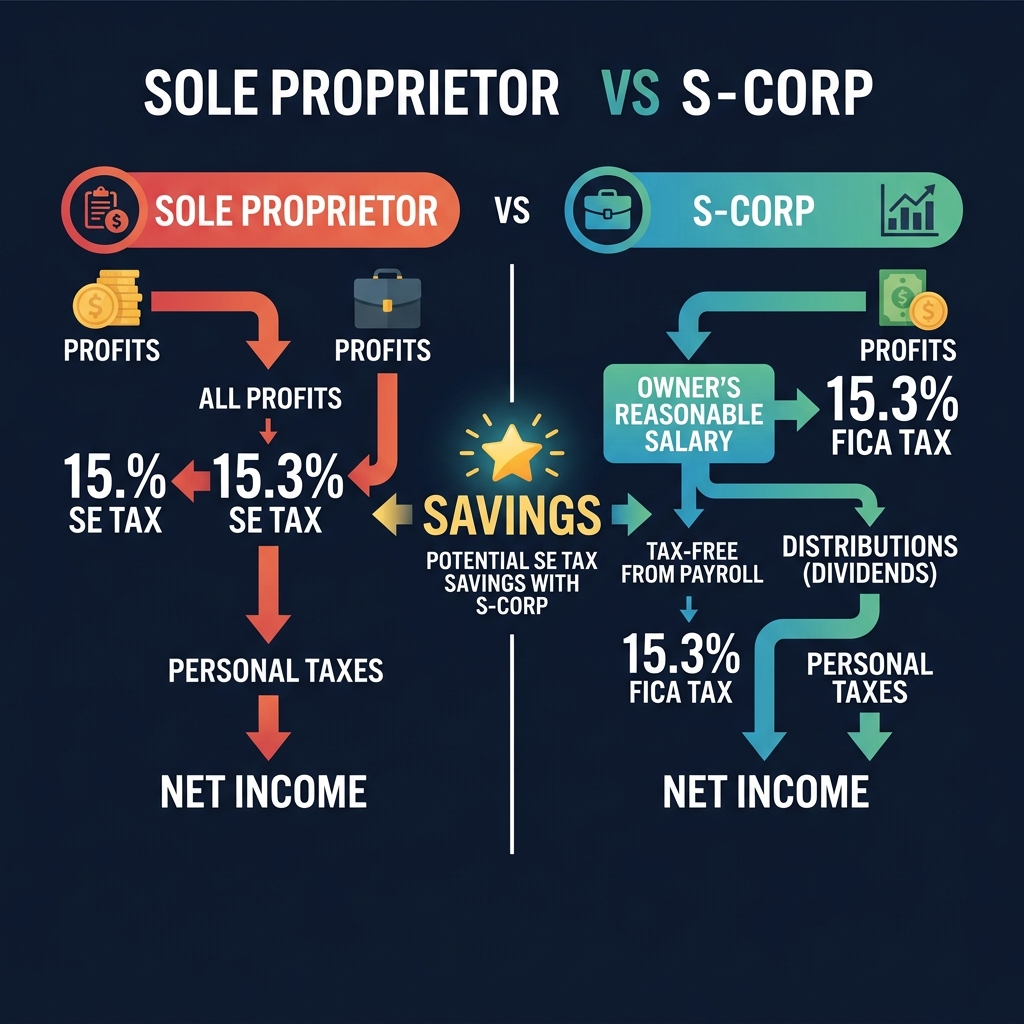

S-Corp vs Sole Proprietorship Tax Comparison

The key advantage of an S-Corp is that only your "reasonable salary" is subject to payroll taxes. Remaining profits flow through as distributions, which avoid the 15.3% self-employment tax.

| Business Profit | S-Corp Salary (60%) | S-Corp Distribution | S-Corp Payroll Tax | Sole Prop SE Tax | Annual Savings |

|---|---|---|---|---|---|

| $60,000.00 | $36,000.00 | $24,000.00 | $5,550.00 | $8,477.73 | $2,927.73 |

| $80,000.00 | $48,000.00 | $32,000.00 | $7,386.00 | $11,303.64 | $3,917.64 |

| $100,000.00 | $60,000.00 | $40,000.00 | $9,222.00 | $14,129.55 | $4,907.55 |

| $120,000.00 | $72,000.00 | $48,000.00 | $11,058.00 | $16,955.46 | $5,897.46 |

| $150,000.00 | $90,000.00 | $60,000.00 | $13,812.00 | $21,194.32 | $7,382.32 |

| $200,000.00 | $120,000.00 | $80,000.00 | $18,402.00 | $27,192.70 | $8,790.70 |

| $250,000.00 | $150,000.00 | $100,000.00 | $22,992.00 | $28,809.65 | $5,817.65 |

| $300,000.00 | $160,000.00 | $140,000.00 | $24,522.00 | $30,564.30 | $6,042.30 |

How S-Corp Payroll Works

What is the S-Corp Tax Advantage?

As a sole proprietor or single-member LLC, you pay 15.3% self-employment tax on all business profits. As an S-Corp:

- You pay yourself a "reasonable salary" — subject to normal payroll taxes (15.3% FICA)

- Remaining profits are taken as S-Corp distributions — NOT subject to self-employment tax

- Both salary and distributions are subject to federal and state income tax

What is a "Reasonable Salary"? Source: IRS.gov

The IRS requires S-Corp owners who provide services to the business to pay themselves a reasonable salary before taking any distributions. "Reasonable" is based on:

- Industry standards — What similar positions pay in your market

- Experience and qualifications — Your skills, education, and track record

- Time and effort — Hours you dedicate to the business

- Revenue and profitability — What the business can realistically afford

S-Corp Payroll Requirements

Once you elect S-Corp status, you must run proper payroll for yourself:

- Get an EIN from the IRS

- Withhold federal and state income taxes from your salary

- Withhold employee FICA (6.2% SS + 1.45% Medicare)

- Pay employer FICA match (another 7.65%)

- Pay FUTA (0.6% on first $7,000)

- File Form 941 quarterly and W-2 annually

When Does S-Corp Make Sense?

S-Corp status typically makes financial sense when:

- Business profits exceed $40,000-$50,000/year

- Tax savings exceed the additional costs (~$500-$2,000/year for payroll service, tax prep, and state fees)

- You can justify a reasonable salary that leaves meaningful distributions

S-Corp Costs to Consider

| Cost | Estimated Annual |

|---|---|

| Payroll service (Gusto, QuickBooks, etc.) | $500-$1,200 |

| Additional tax preparation | $500-$2,000 |

| State S-Corp fees (if applicable) | $0-$800 |

| Registered agent (if required) | $100-$300 |

| Total Annual Overhead | $1,100-$4,300 |

S-Corp Payroll FAQ

Related Tools