Bonus Tax Calculator — How Are Bonuses Taxed? (2026)

See exactly how much tax you'll pay on your bonus. Bonuses are classified as "supplemental wages" by the IRS and are typically withheld at a flat 22% federal rate — higher than many people expect.

Bonus Tax Breakdown (Percentage Method)

The most common method employers use. Your bonus is taxed separately from regular pay at a flat 22% federal withholding rate, plus FICA:

| Bonus Amount | Federal (22%) | Social Security (6.2%) | Medicare (1.45%) | Total Tax | After-Tax Bonus |

|---|---|---|---|---|---|

| $1,000.00 | $220.00 | $62.00 | $14.50 | $296.50 | $703.50 |

| $2,500.00 | $550.00 | $155.00 | $36.25 | $741.25 | $1,758.75 |

| $5,000.00 | $1,100.00 | $310.00 | $72.50 | $1,482.50 | $3,517.50 |

| $7,500.00 | $1,650.00 | $465.00 | $108.75 | $2,223.75 | $5,276.25 |

| $10,000.00 | $2,200.00 | $620.00 | $145.00 | $2,965.00 | $7,035.00 |

| $15,000.00 | $3,300.00 | $930.00 | $217.50 | $4,447.50 | $10,552.50 |

| $20,000.00 | $4,400.00 | $1,240.00 | $290.00 | $5,930.00 | $14,070.00 |

| $25,000.00 | $5,500.00 | $1,550.00 | $362.50 | $7,412.50 | $17,587.50 |

| $50,000.00 | $11,000.00 | $3,100.00 | $725.00 | $14,825.00 | $35,175.00 |

| $100,000.00 | $22,000.00 | $6,200.00 | $1,450.00 | $29,650.00 | $70,350.00 |

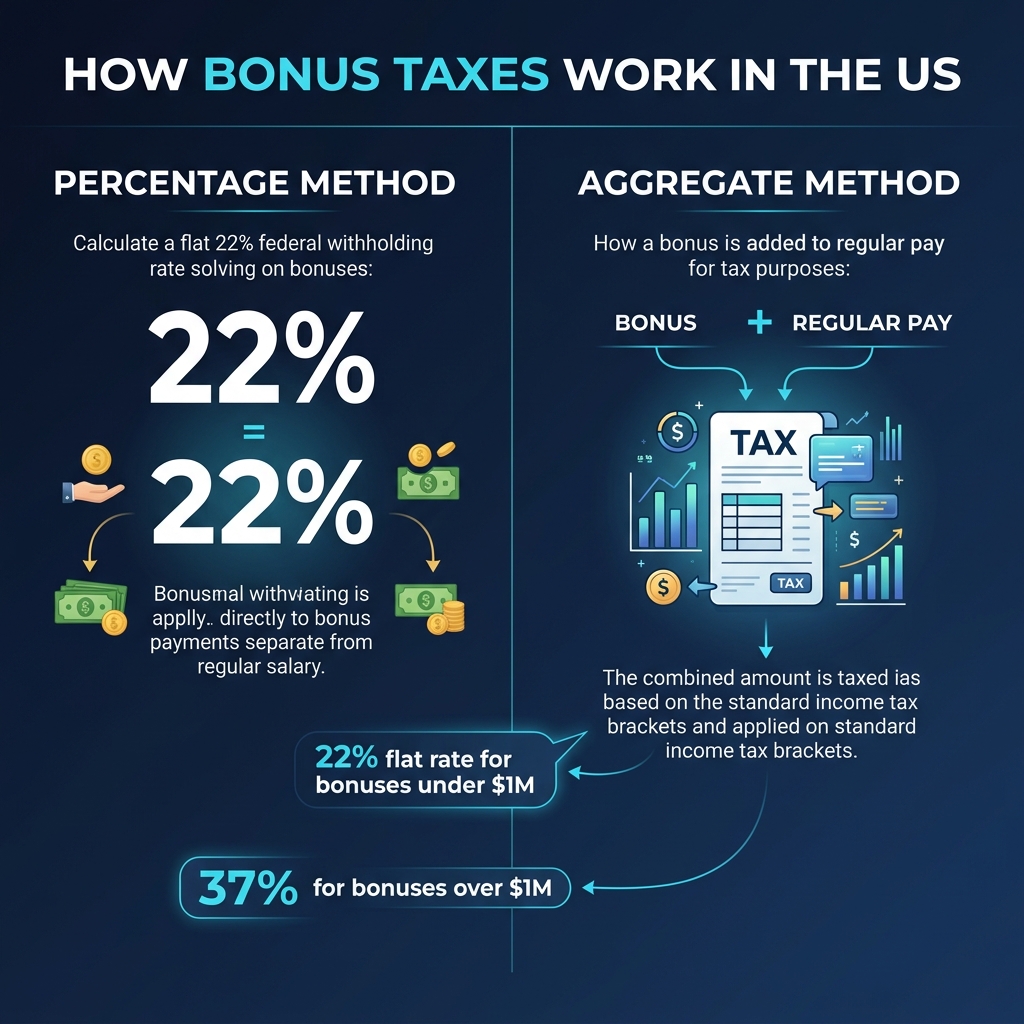

Two Methods for Taxing Bonuses Source: IRS Pub 15

Method 1: Percentage Method (Most Common)

Your employer withholds a flat 22% from the bonus for federal income tax. This is the simpler method and is used by most employers.

- Bonuses under $1 million: 22% flat rate

- Bonuses over $1 million: 22% on first $1M + 37% on excess

Method 2: Aggregate Method

Your employer adds the bonus to your regular paycheck and calculates total withholding as if the combined amount is your normal pay. This often results in higher withholding because the bonus temporarily pushes you into a higher tax bracket.

Important: Withholding ≠ Tax

The 22% flat rate is a withholding rate, not a tax rate. Bonuses are taxed as ordinary income at your marginal tax rate when you file. If you're in the 12% bracket, you may get a refund. If you're in the 32%+ bracket, you may owe more.

Bonus Impact by Tax Bracket

Here's how a $10,000 bonus is actually taxed at filing time (vs. withholding):

| Tax Bracket | Withheld (22%) | Actual Tax | Refund/(Owed) |

|---|---|---|---|

| 10% | $2,200.00 | $1,000.00 | +$1,200.00 refund |

| 12% | $2,200.00 | $1,200.00 | +$1,000.00 refund |

| 22% | $2,200.00 | $2,200.00 | Even |

| 24% | $2,200.00 | $2,400.00 | -$200.00 owed |

| 32% | $2,200.00 | $3,200.00 | -$1,000.00 owed |

| 37% | $2,200.00 | $3,700.00 | -$1,500.00 owed |

How to Keep More of Your Bonus

- Increase 401(k) contributions: Ask your employer to route part of your bonus to your 401(k) — this reduces the taxable amount

- Contribute to HSA: If eligible, pre-tax HSA contributions reduce your taxable bonus income

- Adjust W-4 allowances: If you expect a large bonus, temporarily increase withholding on regular paychecks to avoid owing at tax time

- Time your bonus: If possible, receiving your bonus in January vs December could shift it to a lower-income tax year

Bonus Tax FAQ

Related Tools